Swing Trading Algorithms

Capture Multi-Day Moves

Algorithms optimized for holding positions over multiple days to weeks. These strategies identify trend reversals and continuation patterns, allowing traders to capture larger price movements with fewer trades.

- Larger profit targets

- Less screen time required

- Lower transaction costs

- Works with part-time trading

- Part-time traders

- Position traders

- Those preferring less frequent trades

- Markets with clear trends

Available Swing Trading Algorithms

The RSG Algorithm identifies and trades within established price ranges by detecting support and resistance zones and executing mean-reversion trades when price approaches these levels. The system includes optional grid-based scaling for position building.

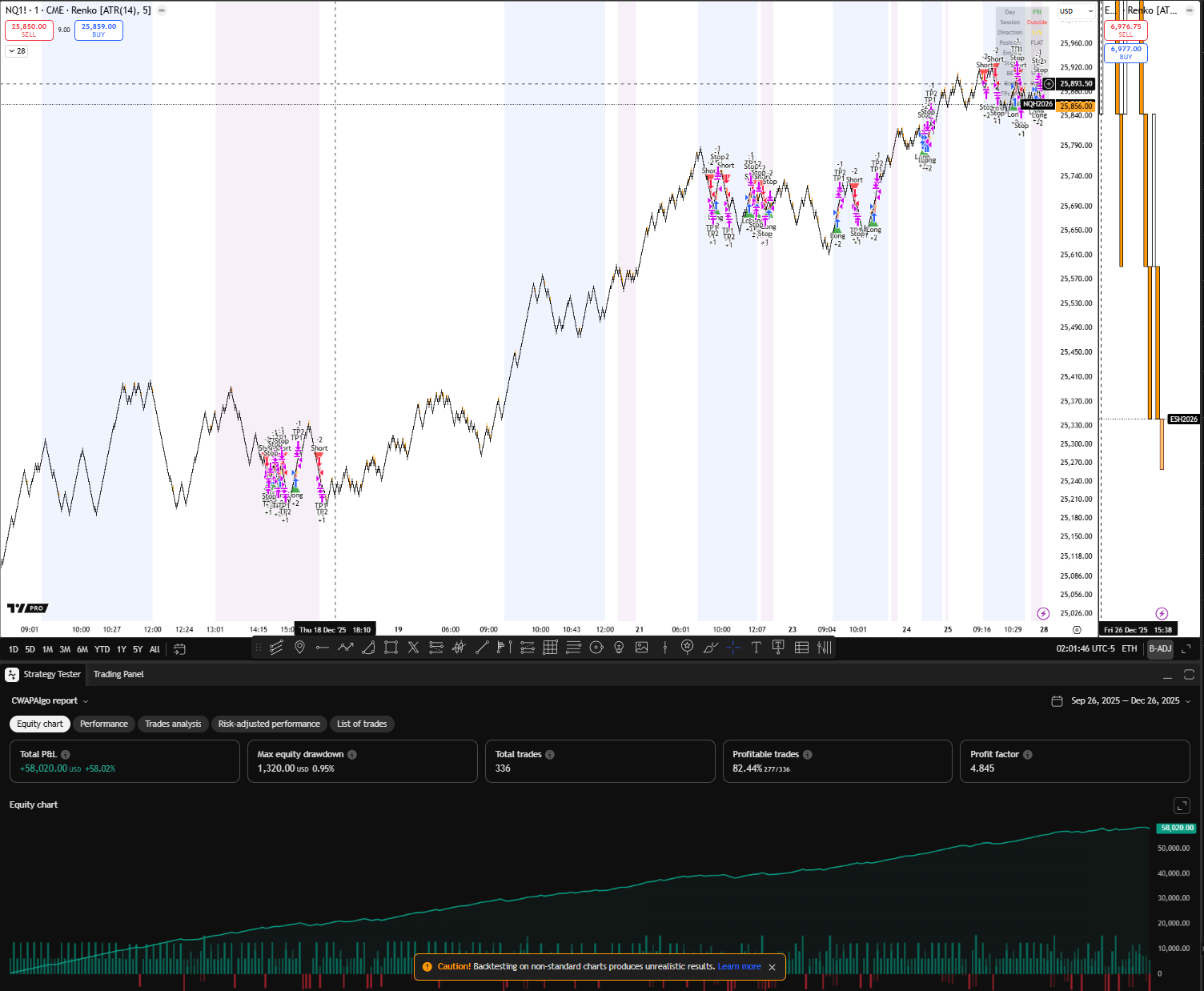

The CWAP Algorithm uses VWAP (Volume Weighted Average Price) as the anchor for institutional fair value and trades deviations from this level. VWAP represents the average price weighted by volume—where institutions benchmark their execution.

The Springboard Algorithm identifies momentum coiling patterns where price consolidates against a key level before "springing" in the opposite direction. The system detects compression of momentum indicators followed by rapid expansion—like a coiled spring releasing stored energy.

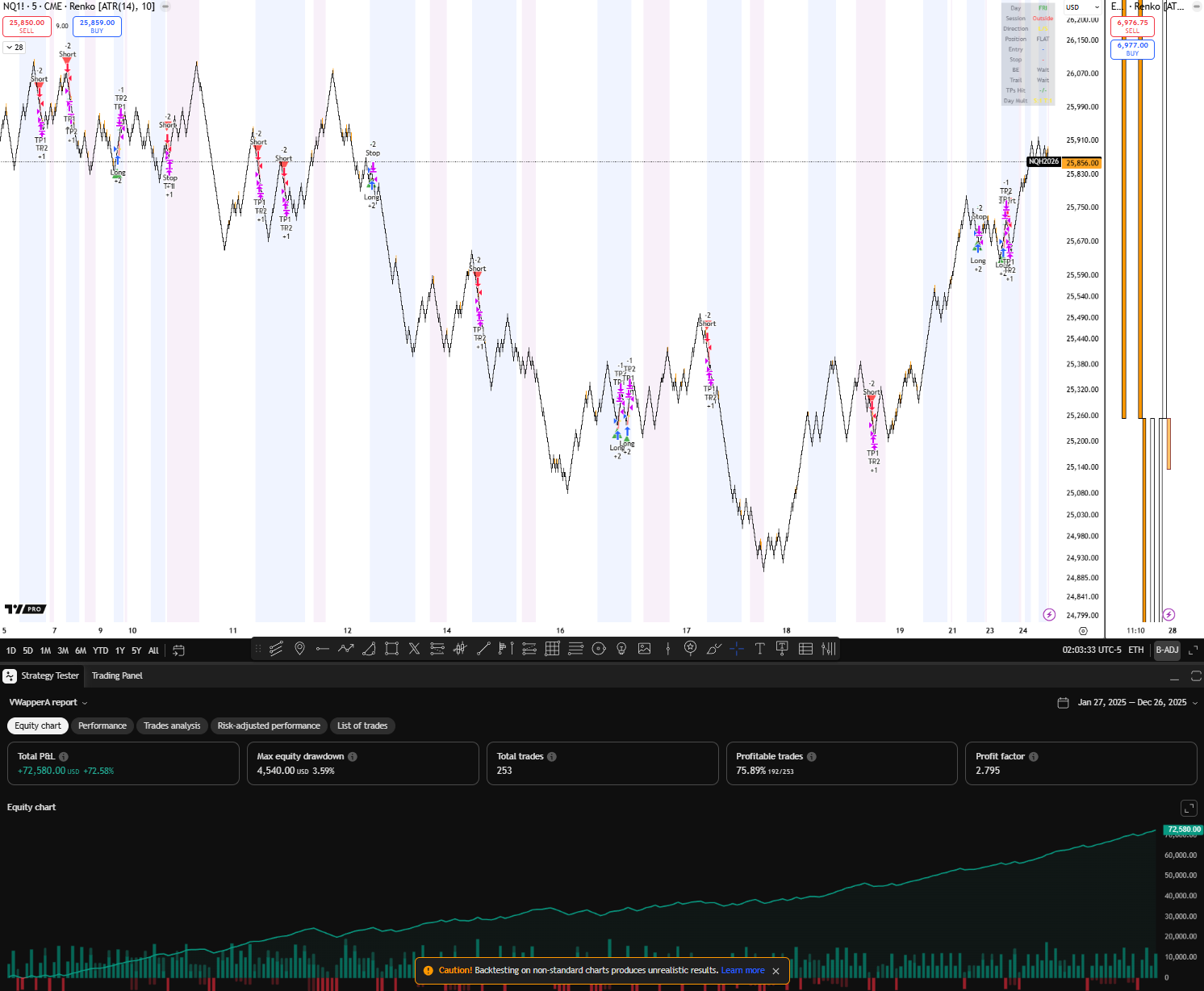

The VWapper Algorithm extends basic VWAP trading with multiple anchored VWAPs, deviation bands, and advanced entry timing. The system uses VWAP as an institutional benchmark while adding sophisticated entry filters.

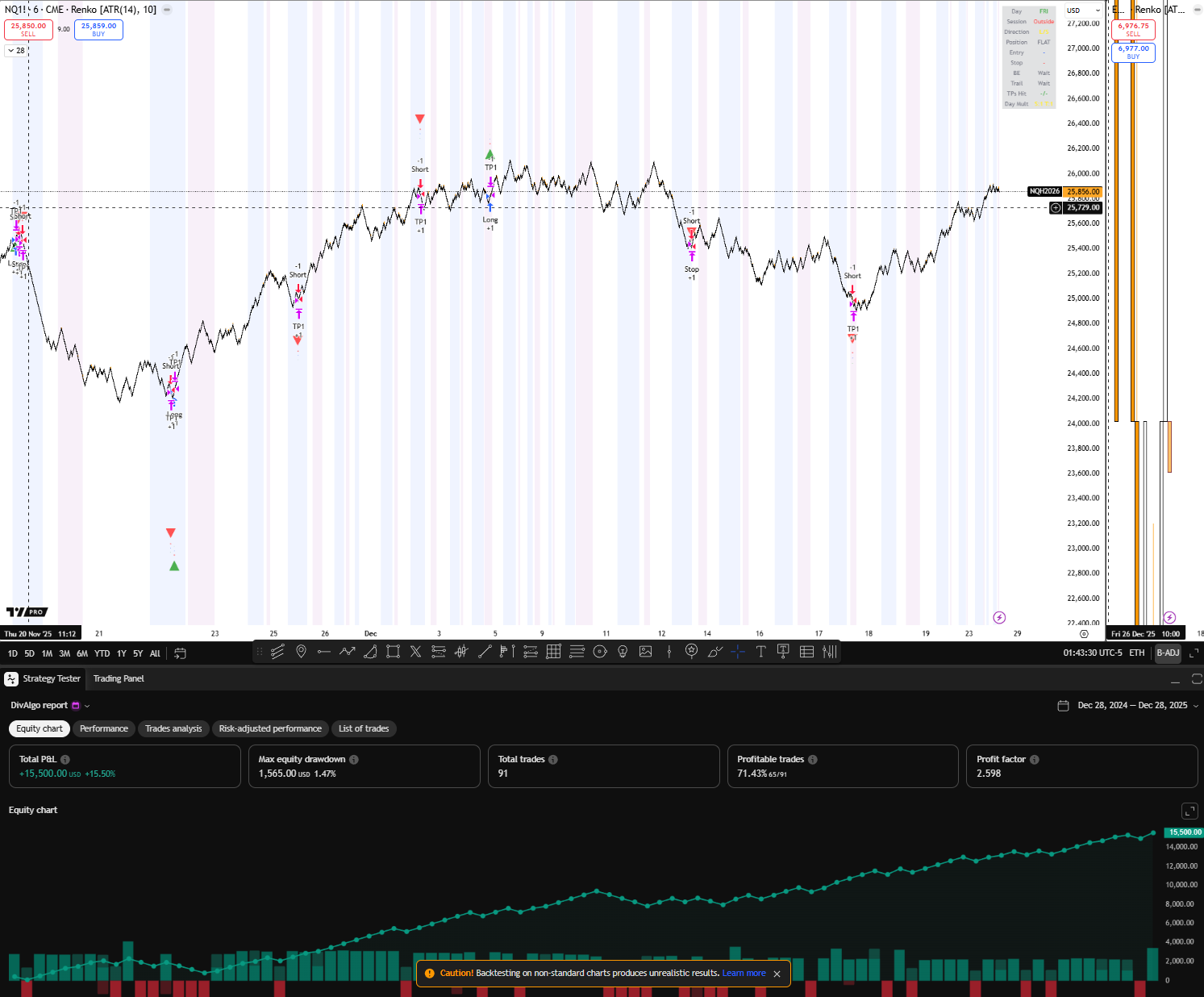

The DivAlgo identifies divergences between price action and momentum oscillators —a powerful signal that often precedes significant reversals. The algorithm supports multiple oscillators (RSI, MACD, Stochastic, CCI) and detects both regular and hidden divergences.

Explore Other Trading Styles

We Value Your Privacy

We use cookies to enhance your browsing experience, analyze site traffic, and personalize content. By clicking "Accept All", you consent to our use of cookies. Read our Privacy Policy for more information.