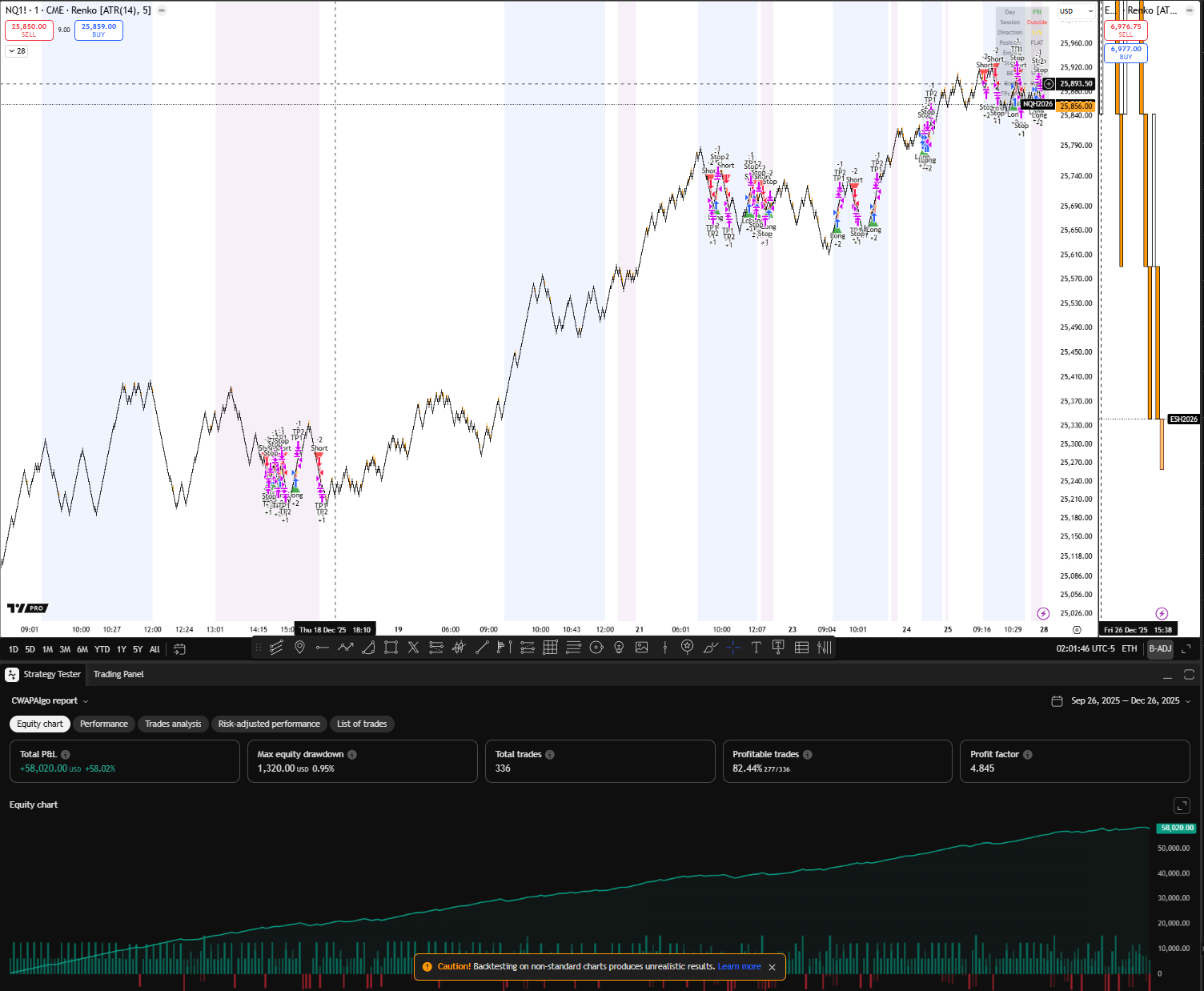

CWAPAlgo

The CWAP Algorithm uses VWAP (Volume Weighted Average Price) as the anchor for institutional fair value and trades deviations from this level. VWAP represents the average price weighted by volume—where institutions benchmark their execution.

About This Algorithm

CUMULATIVE VWAP STRATEGY

Quick Facts:

- Category: VWAP / Institutional

- Markets: Intraday markets

- Timeframes: 5min, 15min, 1H

Overview

The CWAP Algorithm uses VWAP (Volume Weighted Average Price) as the anchor for institutional fair value and trades deviations from this level. VWAP represents the average price weighted by volume—where institutions benchmark their execution.

The system tracks price position relative to VWAP and standard deviation bands, trading mean reversion and VWAP crosses.

How It Works

VWAP CALCULATION Standard VWAP with bands:

- VWAP: Cumulative(Price × Volume) / Cumulative(Volume)

- Upper Band: VWAP + (StdDev × multiplier)

- Lower Band: VWAP - (StdDev × multiplier)

ENTRY MODES

MEAN REVERSION:

- Long: Price at lower band, reverting to VWAP

- Short: Price at upper band, reverting to VWAP

VWAP CROSS:

- Long: Price crosses above VWAP

- Short: Price crosses below VWAP

VWAP BOUNCE:

- Long: Price bounces off VWAP from above (support)

- Short: Price rejects at VWAP from below (resistance)

SESSION HANDLING VWAP resets each session:

- Configurable session start time

- Optional: Use anchored VWAP (custom start)

Key Parameters

VWAP:

- vwapSource ("hlc3"): VWAP price source

- bandMultiplier (2.0): StdDev multiplier for bands

- resetSession (true): Reset VWAP each session

ENTRY:

- entryMode ("MeanReversion"): "MeanReversion", "Cross", "Bounce"

- bandTolerance (0.1): ATR buffer for band touch

SESSION:

- sessionStart ("0930"): Session start time

- timezone ("America/New_York"): Session timezone

Best Use Cases

✅ INTRADAY VWAP trading ✅ INSTITUTIONAL LEVEL trading ✅ MEAN REVERSION to fair value ✅ VWAP BAND extremes

Customer Reviews

Subscribe to Specialty Suite or higher to access

One-Time Purchase

Own the complete Pine Script source code forever. Modify, customize, and use it on your own TradingView account.

What you get with source code:

- Complete Pine Script v5 source code

- Lifetime ownership - no recurring fees

- Full customization rights

- Use on your own TradingView account

We Value Your Privacy

We use cookies to enhance your browsing experience, analyze site traffic, and personalize content. By clicking "Accept All", you consent to our use of cookies. Read our Privacy Policy for more information.